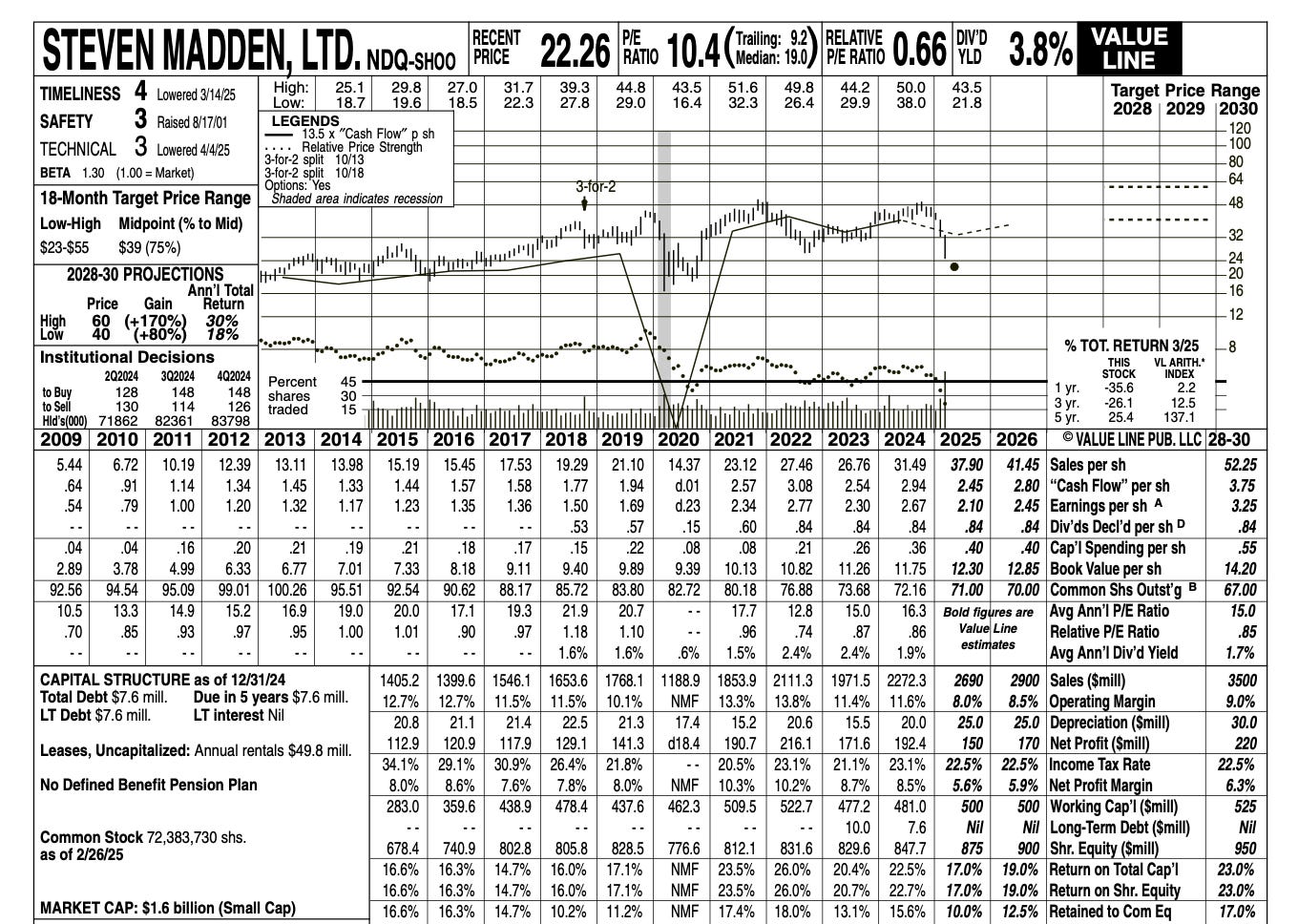

Price: $22.94

Share outstanding: 72.58 million

Market cap: $1.66 billion

Enterprise Value: $1.68 billion

Steven Madden, Ltd. (SHOO) designs and sells fashionable women's shoes, accessories, and apparel at accessible price points. The company has a solid balance sheet, consistently earns high returns on capital (15%+), produces free cash flow ($163.19 million LTM), and buys back stock – share count is down 22% over the past decade. Despite a long history of business success, tariff concerns cut the stock in half. Steve Madden trades for 8.93x earnings (trailing) and offers a 3.52% dividend yield. 3G Capital recently acquired Skechers for 15x earnings.

To start, it’s well to bear in mind some history of the business. In 1990, Steve Madden, a college dropout and shoe store employee, struck out on his own. With $1,100, the young, hyperactive “cobbler” started selling shoes from his car trunk in Manhattan, New York. One of those early shoes was the “Mary Lou”, a variation of the “Mary Jane” produced by the Brown Shoe Company – a Berkshire Hathaway subsidiary – and it was a homerun. In 1993, Steve Madden opened its first retail store, and Stratton Oakmont (from The Wolf of Wall Street) took the company public.

Madden was now rich, but greedy. Stock manipulation schemes with Stratton landed him in prison. Sentenced to forty-one months, Madden served two and a half years and has been righting his wrongs ever since. He kicked his drug addiction, hired some of his prison mates (one became a store manager), and led the company to enormous success.

The company should continue to perform well for a few reasons:

1) Speed and scale. Since day one, the “test-and-react” strategy has been their bread and butter. Steve Madden doesn’t place large bets on future fashion trends. Rather, they knock off more expensive, proven designs and roll out cheaper prototypes to their website (stevemadden.com) and 314 retail stores. Then, customer data is processed. The best-selling products are mass-produced, distributed to a couple of thousand retail stores (Nordstrom, Macy’s, Dillard’s, etc.) in weeks, and are purchased by young, style-conscious, cost-aware women. As a result, inventory turns are industry-leading, and gross margins have been steady, hovering around 40%.

Inventory turns (2024):

Steve Madden: 5.5x

Crocs: 4.6x

Skechers: 4.5x

Wolverine Worldwide: 3.2x

Deckers Outdoor: 3.8x

Genesco: 2.9x

On Holding: 2.3x

Birkenstock: 1.2x

2) A strong niche brand. For nearly four decades, the company’s products have made girls feel stylish without draining their bank accounts. I recently watched “Steve Madden on his sole focus”, a CBS Sunday Morning segment from 11 years ago. A Steve Madden shopper was interviewed and said, “I probably have twenty pairs of Steve Madden shoes”. When customers are complimented on their Steve Madden shoes, they shop there again, and it becomes a habit.

In addition, Steve Madden’s customer loyalty doesn’t rely on a specific celebrity, resulting in greater predictability and less wasteful marketing spend. However, while forgoing large endorsement deals, Steve Madden still finds its way into celebrity wardrobes. The website: www.starstyle.com – tracks celebrity outfits, strutting around in Steve Madden merch — Lady Gaga, Gwen Stefani, Selena Gomez, Demi Lovato, Carrie Underwood, etc. — who have massive fan bases on social media. Selena Gomez takes the lead on Instagram with 420 million followers, equating to 5.12% of Earth’s population!

3) Intelligent capital allocation. Ed Rosenfeld joined Steve Madden in 2005 and became CEO in 2008. Before joining Steve Madden, Rosenfeld worked as an investment banker for Peter J. Solomon, specializing in the retail and apparel industry. Rosenfeld loves buybacks. Steve Madden’s treasury stock amounts to $1.5 billion, with retained earnings at $1.8 billion. EPS has grown 117% over the past decade, and last year's return on tangible equity was 32.3%. Historically, the balance sheet has been solid, with ample cash and zero debt.

Steve Madden, however, just acquired Kurt Geiger for $384.14 million, a UK handbag company with $530 million in revenue, from Cinven, a private equity firm. (Cinven bought Kurt Geiger for $372 million in 2015 from Sycamore Partners.) The deal was financed by a $300 million term loan, and as part of the credit agreement, Steve Madden has a $250 million revolving credit facility. The debt shouldn’t be an issue due to the company’s significant cash flow production.

Kurt Geiger is Steve Madden’s largest deal ever, surpassing all of its past acquisitions combined. For the twelve months ended February 1, 2025, Kurt Geiger generated $530 million in revenue, assuming 8-10% operating margins, that’s $42.4 million to $53 million of operating income. Paying around 8 times earnings (before interest and taxes) for an international, growing company seems like a good deal.

Steve Madden could get acquired, too. According to Steve Madden himself, he’s in his “8th inning” and will retire soon. Madden and Rosenfeld own 3.46% and 1.39% of the company, valued at $58.8 million and $23.6 million. Six months ago, their stakes were worth twice as much, and earlier this week, 3G Capital acquired Sketchers for $9.4 billion at 15x earnings.

Comps – P/E multiples (trailing)

ONON: 60.6x

BIRK: 36.7x

DECK: 20.4x

WWW: 17.9x

CROX: 8.40x

I get that Stratton Oakmont was tacky and annoyed the feds, but SHOO was a good investment so who was the victim?