Cipher Pharmaceuticals $CPH.TO

Cipher Pharmaceuticals $CPH.TO

acne, nail fungus, lice, and scabies

Price: $13.18

Shares Outstanding: 25.59M

Market Cap: $340M

“Cipher Pharmaceuticals” sounds like another speculative biotech company burning cash by the day, and if you look at the stock’s chart it seems like more of a short candidate than a long-term proposition.

“It’s at all-time highs” … “Pharma is out of my circle of competence” … “It’s consensus on X and has amassed a cult following” … I understand the biases and rationale behind this stock giving some “value” investors the “ick”. It’s uncommon for a pharmaceutical company at its all-time high to yield substantial value, but Cipher is the exception. After all, it is a bit counterproductive to completely disregard a given security based on price fluctuations during an orbit; it’s unbusinesslike.

As for the circle of competence, I often ruminate where mine begins and ends. After reading about Cipher’s main drug “Epuris”, a market-leading oral tablet for nodular acne in Canada, I remembered my high school days taking Accutane and intuitively felt within my circumference. I’m not a dermatology expert, but I can understand the data, the consistent cash flow production, the people running the business, and their track record. The stock was much cheaper when it was trading at 2x acne earnings, though less diversified.

Lastly, the cult argument is the weakest. There are good investors on X with solid ideas, it’s only natural for a larger cohort of investors to agree on a company that continues to perform well fundamentally.

More on Cipher:

Cipher Pharmaceuticals ($CPH.TO), based in Oakville, Canada, operates an asset-light business model focused on cash generation. Instead of investing in R&D, the company acquires and licenses products, freeing up capital for M&A and returns. Its two main segments are the Product Segment (sales in Canada, 60% of revenues) and the Licensing Segment (royalties from U.S. licensing agreements, 40% of revenues). Insiders own 40% of the company, and CEO Craig Mull is a great manager and capital allocator.

Despite the stock's multi-bagger run-up, it could double again over the next several years due to the following:

Sun Pharmaceuticals license expiration, Cipher taking Absorica in-house will about double earnings.

MOB-015 (nail fungus topical) license is set to take over the Canadian market, as the current topical (Jublia with 90% market share) is not nearly as effective. Canada's market for onychomycosis is around $100 million, and Cipher thinks they can take it. $50 million of cash flow is possible.

The recent acquisition of Natroba (lice and scabies) from ParaPro, which is doing $11 million of EBITDA with 20’s% market share. There’s still the US to capture + license revenue overseas. This can be a $50 million cash-flowing asset.

The management team will aggressively bid for a MOB-015 license in the United States from Moberg Pharma. The nail fungus topical grew the market in Sweden by 50% in 1 month. If Mull gets this license he cements himself in the micro-cap hall of fame.

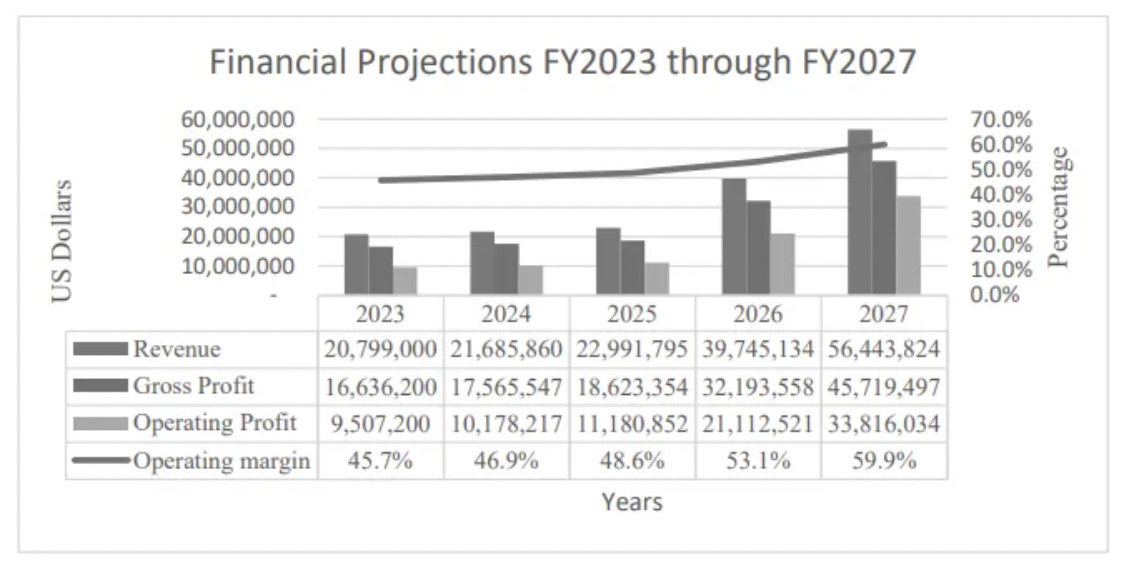

The picture attached is management’s projection of earnings through FY 2027 for their NCIB (normal course issuer bid, which is share repurchases) in 2023.

These are projected earnings before the Natroba acquisition, taking Absorica in-house, and securing the MOB-015 license in the US. The cash flows of current products are stable and act as a backstop on valuation.

Epuris & Absorica:

Cipher’s key product is CIP-Isotretinoin, sold as Epuris in Canada and Absorica in the U.S. Epuris leads the Canadian market with 46% share and stable, growing demand due to its advantages over competitors, mainly because it can be taken without eating food beforehand (popular among young girls). Despite the licensing segment's declining sales due to generic competition for Absorica in the U.S., growth in Epuris has stabilized overall revenues. Additionally, recent amendments to the Absorica licensing agreement have reversed its sales decline, contributing to renewed growth. The Licensing Segment also includes products like Lipofen and newer agreements for Epuris in Mexico. In the last six months, Absorica generated revenues of $3 million, and Epuris produced $6 million in revenue.

MOB-015 (Moberg Pharma):

MOB-015, developed by Swedish company Moberg Pharma ($MOB.ST), is a treatment for Onychomycosis (nail fungus), and Cipher owns Canadian rights. Two key points highlight its potential.

First, the likelihood of success is strong. While drug development always carries risk, MOB-015 has been recommended for approval in 13 European countries after showing a 76% mycological cure rate compared to 42% in competing treatments. Europeans have been raving about the product, and it grew the Swedish market by 50%. It's currently in Phase 3 trials in North America, with results due by January 2025. Although earlier trials met all clinical endpoints, they caused unwanted nail discoloration. This issue is being addressed with a lower dose, increasing the chances of approval. Given the drug's European approval and manageable issues, expectations are high, reflected in Moberg’s stock performance, which has surged from single digits to 28 SEK per share since mid-2023. Cipher values the Canadian Onychomycosis market at CAD 82 million, projected to grow 8% annually through 2030, where Bausch’s Jublia currently dominates with a 90% market share. Moreover, Mull has been adamant about acquiring the US license.

Natroba (ParaPro):

Cipher Pharmaceuticals has undergone a major transformation since its recent acquisition of Natroba, a dermatology product for lice and scabies, for $89.5 million. The risk of management making an acquisition blunder has subsided, and quite the opposite occurred. This deal has doubled Cipher’s earnings, boosting its stock by 100% and returning 150% over the past six months. Despite the rise, the stock remains attractive, with the company now trading at around 15x cash flow—still relatively low given the growth potential.

Natroba presents significant growth opportunities, particularly in the US, where its current market share is only 22%, compared to 70% for permethrin. However, permethrin’s declining effectiveness, now estimated at around 30%, offers room for Natroba to expand, especially since it has patent protection until 2033. Beyond the US, Cipher plans to seek approval for Natroba in Canada and is in talks to out-license the product in Europe, providing additional growth avenues.

I recommend giving the Framp Files a read.

The acquisition also brings Cipher new infrastructure, including a US sales team and headquarters, positioning the company to bring Absorica in-house once its licensing deal with Sun expires in 2024. This move could add $10 million in incremental cash flow. Additionally, Cipher may use this new infrastructure for future acquisitions and expand its US market presence.

Cipher’s acquisition of Natroba not only diversifies its product portfolio but also reduces its reliance on isotretinoin, which was previously a major revenue driver. With the added scale and liquidity, Cipher is now a much more investable company, having transitioned from a cash-rich, overcapitalized entity to a growth stock. Mull is intent on growing Cipher Pharmaceuticals into a $1 billion company, and is aiming for a US listing.

Looking ahead, Cipher’s operating income could grow substantially, potentially reaching $60+ million in the next few years, driven by Natroba and MOB-015’s growth, Absorica’s in-housing, and other strategic moves. Even in a worst-case scenario, Cipher remains a strong asset-light, cash-generative business with manageable leverage led by a prudent capital allocator with skin in the game.

Recommended readings:

https://valueinvestorsclub.com/idea/CIPHER_PHARMACEUTICALS_INC/1631639401

https://substack.com/@frampypants92

Cipher Pharmaceuticals management interviews:

Note on $MOB.ST: At today’s price, the investor is buying cash flows of a nail fungus topical that could become the standard cure for onychomycosis. The company practically sold a nail polish asset for $155 million. Cipher is a much safer bet with a higher likelihood of success, a diverse cash-generative product line with outstanding management. Moberg provides the polar opposite, a subpar CEO with a single asset banking on a successful phase 3 trial in the US.

Hi, thanks for the overview. Much appreciated.

As this post was published yesterday, I guess you could add a comment on the warning by Moberg regarding lowered expectations for the ongoing phase 3 trial.

Personally, I think it affects mich more Moberg than Cipher which suffered a sympathetic, but dampened, sell off